Why China Is Investing Billions in Brazil

The global economy is entering a new kind of resource race. Oil still matters, but the minerals powering electric vehicles, batteries, renewable energy systems and advanced electronics are becoming just as strategic.

Governments and corporations around the world are competing to secure access to lithium, nickel, graphite, copper, cobalt and rare earth elements.

In this new landscape, Brazil is becoming increasingly important.

Chinese companies recognized this early. In 2025, Chinese mining investments in Brazil more than tripled, reaching approximately US$ 1.76 billion.

The scale and speed of the expansion reflect how central Brazil has become to the global energy transition.

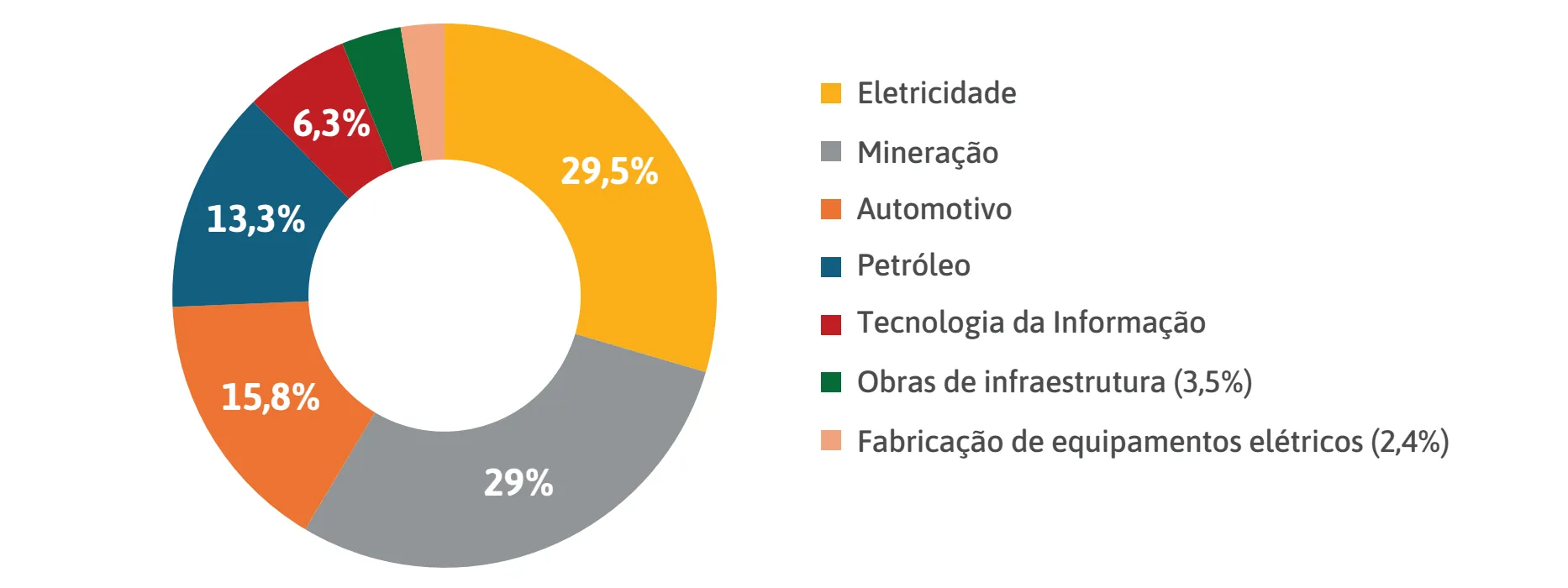

China invests mostly in Electricity, Minerals and automotive in China.

The New Resource Race

For decades, Chinese investment in Latin America focused heavily on oil, infrastructure and agriculture. Mining has now returned to the center of the relationship, but with a very different logic than before.

Today, the focus is closely tied to electrification, battery production and decarbonization.

Electric vehicles require dramatically larger amounts of critical minerals than conventional gasoline vehicles. Renewable energy infrastructure also depends heavily on mineral-intensive supply chains.

Wind turbines, transmission systems, solar installations and battery storage all consume large quantities of processed metals and rare materials.

China dominates much of the global processing capacity for these materials, but it still relies heavily on imported raw materials. Securing long-term supply therefore became a strategic priority for Chinese industry.

Why Brazil Matters

Brazil offers an unusual combination of advantages.

The country possesses enormous reserves of several minerals considered essential for the future low-carbon economy. Brazil holds roughly 26.5 percent of global graphite reserves and is the second-largest holder of rare earth reserves worldwide.

It also possesses major nickel, bauxite and other strategic mineral reserves.

Unlike some neighboring countries that depend heavily on a single mineral category, Brazil offers diversification.

Chile and Argentina are strongly associated with lithium. Peru dominates in copper. Brazil combines multiple strategic resources together with a large industrial economy and significant renewable energy potential.

Chinese Mining Companies Expand Aggressively

Chinese companies have responded aggressively.

In one of the largest transactions of 2025, CMOC acquired gold mining assets from Equinox Gold in a deal worth around US$ 1 billion.

MMG Singapore Resources purchased Anglo American’s nickel business in Brazil for roughly US$ 500 million.

Baiyin Nonferrous entered Brazil through the acquisition of Mineração Vale Verde, focusing on copper production.

These investments are not simply financial transactions. They are strategic moves aimed at securing future supply chains linked to batteries, electric vehicles, renewable energy systems and industrial manufacturing.

The EV Supply Chain Connection

The relationship between mining and manufacturing is becoming increasingly integrated.

Chinese electric vehicle manufacturers are simultaneously expanding production capacity in Brazil. BYD, GWM and Geely are all increasing their local presence.

This creates the possibility of developing regional supply chains that connect Brazilian mining directly to vehicle manufacturing and eventually to broader Latin American markets.

In many ways, Brazil is evolving into a strategic platform rather than just a resource supplier.

Renewable Energy and Industrial Expansion

Renewable energy plays a central role in this transformation.

Chinese investments in Brazilian electricity projects reached record levels in 2025, particularly in solar, wind and transmission infrastructure.

The growth of renewable energy capacity strengthens Brazil’s attractiveness for industrial production, especially for manufacturers facing increasing pressure to reduce emissions across their supply chains.

This creates a reinforcing cycle.

Renewable energy supports industrial expansion. Industrial expansion increases demand for minerals. Mineral production supports battery and electric vehicle manufacturing.

Challenges and Risks

Brazil still faces serious challenges.

Mining projects often encounter environmental licensing delays, infrastructure bottlenecks and political uncertainty. Logistics costs remain high in many regions.

Environmental concerns are particularly sensitive in parts of northern Brazil and the Amazon region.

Western governments increasingly view critical minerals as strategic assets, and competition for access is intensifying globally.

Opportunities for International Companies

Despite these risks, the long-term trajectory remains clear. Demand for critical minerals is expected to rise for many years as electrification expands worldwide.

Engineering firms, industrial equipment suppliers, automation providers, logistics companies and environmental service firms are all likely to benefit from rising investment across Brazil’s mining and industrial sectors.

There is also growing demand for technologies related to water treatment, energy efficiency, emissions reduction and advanced mineral processing.

Conclusion

Brazil is no longer simply exporting raw materials to China. Increasingly, it is becoming integrated into the industrial systems powering the next generation of energy and transportation technologies.

The countries and companies that position themselves early inside these emerging supply chains are likely to gain major advantages over the next decade.

Can you afford not to enter the Brazilian market? Talk to us, we’ll help you succeed in Brazil.

Talk to us →