Something remarkable is happening in the United States right now: productivity is growing at its fastest pace in two decades. While many are looking to Artificial Intelligence as the answer, the real drivers lie elsewhere — in a combination of an energy boom, economic flexibility, and the delayed payoff from the digital transformation of the last decade.

As with so many economic miracles, observers initially struggled to believe what they were seeing. For an entire decade following the global financial crisis of 2007–09, productivity growth across the Western world appeared clinically dead. Since long-term prosperity ultimately depends on producing more with the same amount of labor, even wealthy America seemed destined for permanent stagnation — not to mention Europe. The Congressional Budget Office (CBO), which had repeatedly overestimated growth during the 2010s, remained consistently pessimistic throughout this decade. Early signs of improvement were dismissed as “false prophets.”

But the data kept delivering. By now, the evidence is undeniable: over the past five years, U.S. productivity has grown faster than at any time in roughly twenty years. Whether measured by output per worker or output per hour, productivity has risen by a healthy 2% annually — compared with a sluggish 1% during the 2010s. This has led the Federal Reserve to raise its estimate for long-term U.S. GDP growth from 1.8% to 2%. Jerome Powell, the outgoing Fed Chair, recently expressed his surprise during a press conference: “I never thought I would spend so many years experiencing truly high productivity,” he said in response to a question from The Economist.

AI Is Not the Savior — At Least Not Yet

It is still too early to give Artificial Intelligence credit for this resurgence. The productivity boom began in the early 2020s, while large language models (LLMs) have only been in meaningful commercial use for about a year. If past technological revolutions are any guide, it may take years before the AI era becomes visible in official productivity statistics. So far, the only clearly measurable macroeconomic impact of the AI boom has been increased corporate investment, particularly in data centers.

So Where Is the Growth Coming From?

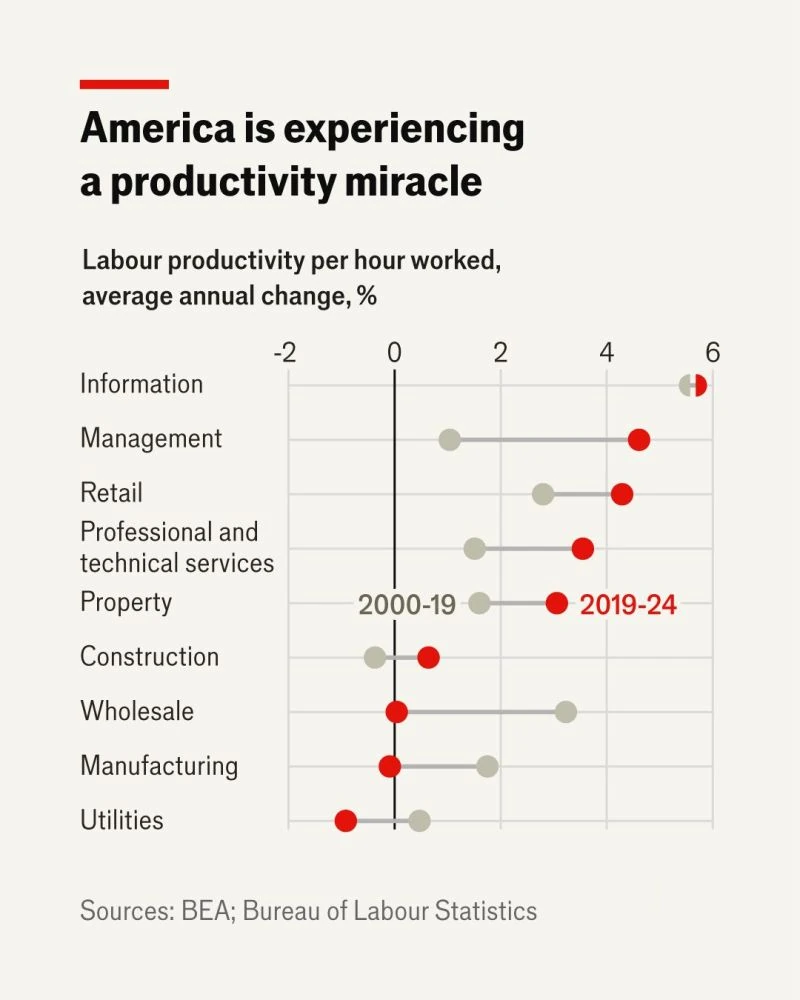

To find the real drivers, it helps to look at sector-level data from the Bureau of Labor Statistics. Between 2019 and 2024, the “information sector” (software, telecommunications, film) led the way with annual growth of 6%, but this is not actually a new trend — it roughly matches the average seen between 2000 and 2019.

The real surprise lies in professional services and management. These sectors account for roughly 10% of the U.S. economy. These are not companies that invent new technologies, but companies that deploy them at scale. In recent years, America’s white-collar workforce has finally begun fully exploiting the innovations of the 2010s: smartphones, cloud computing, and video conferencing are now deeply integrated into daily workflows.

Energy as a Competitive Advantage

Another major driver is the oil and gas sector. The shale revolution transformed the United States from a net energy importer into an exporter. Thanks to new LNG export facilities, America can now ship fuel to Europe and Asia, where prices are often far higher than in the domestic market.

The indirect effects may be even more important: electricity is an input into nearly everything — and Americans pay, on average, only about half as much for power as Europeans and roughly one-third less than Japanese consumers. When energy is cheap and abundant, factories and industrial machinery can operate at full capacity without constant concern over energy costs. This helps explain why energy-intensive industries such as mining and chemicals are thriving in the United States while struggling to survive in Europe.

Flexibility in Times of Crisis

Perhaps the most fundamental factor is the unusual flexibility of the U.S. economy. The beginning of the current boom coincided with the Covid-19 pandemic. Unlike Europe, the United States relied heavily on direct cash support rather than complex job-retention schemes that tied workers to existing employers. Once lockdowns ended, workers were able to move more quickly into new jobs at more productive companies, since the most efficient firms were also the fastest to hire.

Even recent political shocks have so far failed to derail growth. From early 2025 through March 2026, productivity growth remained solid at rates between 1.2% and 2.1% — despite Donald Trump’s tariffs, mass deportations, and attacks on institutions such as the Federal Reserve. It is likely that the economy will also weather the current administration’s broader strategic conflicts.

The Bottom Line: America’s productivity miracle will likely continue. And once the AI era finally begins to show up fully in the statistics, this miracle could evolve into a genuine age of abundance.

Can you afford not to enter the US market? Talk to us, we’ll help you succeed in the United States.

Talk to us →