In the world of infrastructure, some shifts happen quietly, and others arrive with the force of a tectonic plate moving. In May 2024, Brazil sent a signal that barely registered in mainstream tech circles, but effectively rewrote the playbook for AI investment in Latin America: If you want to operate a data center in Brazil, you must build your own power plant.

This isn’t a policy of “green-washing” or mere sustainability. It is a matter of “Infrastructure Math.”

At GMEX Consulting, we track how physical constraints dictate digital growth. Here is why Brazil’s mandate is a preview of the global future for AI and enterprise infrastructure.

The Grid Crisis: AI is No Longer a “Standard” Consumer

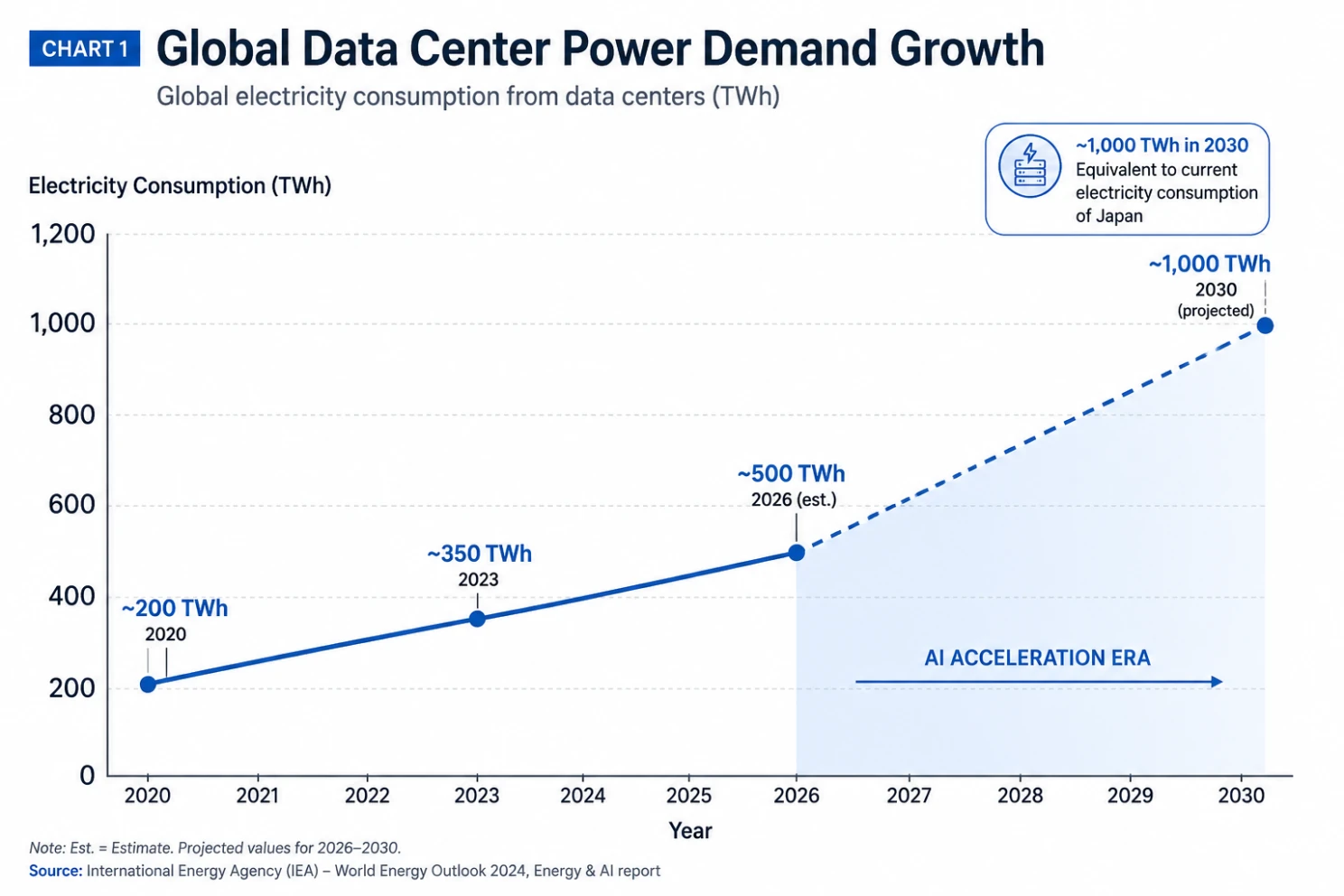

The traditional relationship between a data center and the power grid is broken. A modern AI inference cluster isn’t just another industrial building; it draws between 10 to 50 megawatts (MW) continuously. To put that in perspective, a mid-sized campus can consume as much electricity as a small city.

Most national grids were designed for predictable, steady industrial loads. They cannot absorb massive AI clusters overnight without risking stability. In Brazil—where the grid relies on hydropower for 70% to 80% of its energy—seasonal droughts make the system even more fragile. Adding uncontrolled data center loads to a stretched grid doesn’t just raise prices; it risks destabilization.

Brazil’s answer? Energy Self-Sufficiency.

The Case for Captive Hydro: A 20 MW Model

For a Chief Financial Officer, the idea of building a power plant sounds like “scope creep.” However, the data proves that owning the generation asset is the only way to protect long-term margins.

Consider a 20 MW run-of-river hydroelectric plant in Southern Brazil:

-

Total Capex: Approximately $60M – $65M.

-

The Southern Advantage: Regions like the Paraná River watershed (Rio Grande do Sul and Santa Catarina) offer proven engineering, local EPC expertise, and consistent year-round water flow.

-

Operational Resilience: Run-of-river designs minimize the environmental footprint compared to massive dams while providing a steady base load for AI operations.

The Financial Architecture (The CFO Frame)

When we move beyond the initial capital outlay, the ROI story is compelling:

-

Years 1-4 (Build): Deploying capital into a strategic asset.

-

Years 5-12 (Payback): At current grid prices ($45-$60/MWh), the plant pays for itself through energy savings alone.

-

Years 13-30 (Pure Margin): While competitors are subject to volatile grid pricing and “dry season” surcharges, the self-generating operator has locked in energy at an LCOE (Levelized Cost of Energy) of roughly $35-$45/MWh.

Beyond Brazil: A Global Template

Brazil’s framework is a “canary in the coal mine.” We are already seeing the EU and Southeast Asian markets discuss similar energy self-sufficiency requirements.

The companies that move first to synchronize their compute deployment with their own energy infrastructure will hold a structural cost advantage that later entrants cannot match. At the hyperscaler level (100MW+), this isn’t just about saving money—it’s about the physical ability to exist. You can build a run-of-river hydro plant almost anywhere there is elevation change and consistent water flow. But not every location stacks up economically and logistically. The Paraná River watershed spanning Rio Grande do Sul and Santa Catarina offers several advantages stacked together.

The data center of 2030 will not be a passive utility customer. It will be a sophisticated energy manager that happens to process data.

For enterprise leaders and infrastructure investors, the question is no longer “How much does the power cost?” but rather “Do we own the source?” In the race for AI supremacy, the winners will be those who build their own power.

Are you planning your next infrastructure move in Latin America?

Can you afford not to enter the Brazilian market? Talk to us, we’ll help you succeed in Brazil.

Talk to us →